CORRESP: Correspondence

Published on March 10, 2025

March 10, 2025

VIA EDGAR

U.S. Securities and Exchange Commission

Division of Corporation Finance

100 F. Street, N.E.

Washington, D.C. 20549

| Attention: | Brian McAllister Shannon Buskirk Anuja Majmudar Irene Barberena-Meissner |

| Re: | Namib Minerals, as Registrant (CIK No. 0002026514) | |

| Greenstone Corporation, as Co-Registrant (CIK No. 0002034129) | ||

| Amendment No. 3 to the Registration Statement on Form F-4, Filed February 25, 2025 | ||

| Staff Comment Letter Dated March 3, 2025 |

Ladies and Gentlemen:

This letter is submitted on behalf of our client, Namib Minerals, a foreign private issuer and exempted company limited by shares incorporated under the laws of the Cayman Islands (the “Company”), and its co-registrant, Greenstone Corporation, a foreign private issuer and exempted company limited by shares incorporated under the laws of the Cayman Islands (the “Co-Registrant” or “Greenstone” and, together with the Company, the “Registrants”), in response to the comments of the staff of the Division of Corporation Finance (the “Staff”) of the U.S. Securities and Exchange Commission (the “Commission”) with respect to the Registrants’ Amendment No. 3 to the Registration Statement on Form F-4, filed with the Commission on February 25, 2025 (the “Registration Statement”), as set forth in your letter dated March 3, 2025 addressed to Ibrahima Tall and Tulani Sikwila (the “Comment Letter”). In submitting this response, the Registrants are concurrently filing publicly with the Commission, electronically via EDGAR, Amendment No. 4 to the Registration Statement on Form F-4 (the “Amendment No. 4”), which includes changes that reflect responses to the Staff’s comments.

The Registrants advise the Staff that they seek to finalize the review process as soon as practicable with a view to seeking effectiveness of the Registration Statement during the week of March 10, 2025.

The headings and numbered paragraphs of this letter correspond to those contained in the Comment Letter, and to facilitate your review, the text of the Comment Letter has been reproduced herein, followed by the Company’s response to each comment. Unless otherwise indicated, page references in the descriptions of the Staff’s comments refer to the Registration Statement, and page references in the Company’s responses below refer to the Amendment No. 4.

Greenberg

Traurig, LLP § Attorneys

at Law § WWW.GTLAW.COM

1840 Century Park East, Suite 1900 § Los

Angeles, California 90067-2121 § Tel 310.586.7700 § Fax 310.586.7800

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 2 of 16

Concurrent with the filing of this response letter, the Company is submitting a request for confidential treatment pursuant to Rule 83 under the Securities Act of 1933, as amended (the “Act”), with respect to certain supplemental information provided to the Staff separately in accordance with Rule 418 under such Act to assist in the Staff’s understanding of the Company’s responses below.

In submitting this response to the Staff, the Company is including the following information:

| ● | Part I: Response to Comment Letter, dated March 3, 2025; |

| ● | Part II: Clarification of Response to Comment 1 of the Staff’s comment letter, dated February 18, 2025, as discussed with the Staff; and |

| ● | Appendices. |

Part I: Response to Comment Letter, dated March 3, 2025:

Amendment

No. 3 to Registration Statement on Form F-4

Greenstone Corporation Financial Statements

3.3 Property and equipment, page F-108

Comment 1: We have read your response to comment 1. We understand your inferred resource estimates are primarily based upon the expectation of future upgrades and recoveries and they lack data and information generated by any mineral exploration program. In the absence of adequate geological evidence, your estimates of inferred resources should be excluded from consideration in the determination of the useful life of your mining assets. As a result, please provide the following:

| ● | Tell us how the exclusion of inferred resources impacts your depreciation expense for mining assets under the application of the straight-line and units-of-production methods for the periods presented. |

| ● | Provide us with the results of your calculation of both methods, highlighting the difference between historical depreciation expense and the revised amounts and the impact it has on your results of operations and financial position for the periods presented. |

| ● | Tell us how you reconsidered the application of the units-of-production method rather than the straight-line method and evaluated whether this depreciation method may better reflect the pattern of consumption of future economic benefits, as explained in IAS 16. |

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 3 of 16

Response to Comment 1: The Company acknowledges the Staff’s comment and advises the Staff as follows:

The Company notes that the Staff comments, in relevant part, that “estimates of inferred resources should be excluded from consideration in the determination of the useful life of your mining assets.” For the reasons set forth herein and in Part 2 below, the Company respectfully advises the Staff that it believes the inclusion of estimates of inferred resources in its calculation of the life of its mining assets is appropriate and consistent with the principles set forth in IAS 16, as demonstrated within the computations contained in the confidential supplemental information provided to the Staff under separate cover in reliance upon Rule 418 of the Act. On the basis of the Company’s review and analysis, the Company advises the Staff that:

| ● | For the annual period ended December 31, 2023, use of the units-of-production method as compared to the Company’s straight-line method (both including inferred resources and excluding inferred resources) results in an immaterial difference in the amount of annual depreciation expense and has a similarly immaterial impact on the Company’s statements of financial position and results of operations. With respect to the annual period ended December 31, 2022, use of the units-of-production method as compared to the Company’s straight-line method resulted in a larger difference in annual depreciation as compared to the results in 2023. The difference was due to breakdowns of critical mining equipment which occurred in the first quarter of 2022 and impacted the level of production. The length of time required to restore the equipment and restore normal levels of production was longer than the typical recovery time due to the impact on the supply chain from the COVID-19 pandemic. Under normal circumstances, the typical recovery time is less than 10 days and therefore does not result in a significant impact on the level of production. |

| ● | IAS 16 indicates the depreciation method should reflect the pattern in which the asset’s future economic benefits are expected to be consumed and provides that a variety of depreciation methods may be used, thereby providing flexibility given the facts and circumstances of the particular entity/assets. |

| ● | As described in the Company’s response letter of February 4, 2025, the Company maintains relatively consistent levels of production across annual periods in line with plant capacity, and thus the straight-line method of depreciation allocates roughly an equal amount of depreciation to each unit produced in a manner similar to the units-of-production method and serves as a reasonable basis to conclude the appropriateness of utilizing the straight-line method. |

As a result, the Company asserts that the straight-line method of depreciation sufficiently reflects the pattern of consumption and matching of costs and benefits as described in paragraph 60 through 62 of IAS 16.

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 4 of 16

Namib Minerals

Audited Financial Statements, page F-137

Comment 2: Please update to include the subsequent interim financial statements of at least the first six months of the financial year. We refer you to Item 8.A.5 of the requirements to Form 20-F.

Response to Comment 2: The Company advises the Staff that the Namib Minerals’ unaudited interim financial statement as of and for the period from inception (May 27, 2024) to June 30, 2024, and notes thereto, have been included in Amendment No. 4, as filed with the Commission on March 10, 2025.

Part II: Clarification of Response to Comment 1 of the Staff’s comment letter, dated February 18, 2025, as discussed with the Staff:

The Company thanks the Staff for its time and consideration since the issuance of the Comment Letter in facilitating the Company’s ability to discuss directly the Staff’s questions with respect to the inclusion of the inferred resources in the life of mine (“LoM”) calculation. As noted to the Staff in such discussions, the Company considers that its prior response to the Staff’s letter of February 18, 2025, comment 1, warrants additional explanation in light of further discussion and review. As a result, the Company supplementally incorporates below a more detailed and robust explanation of its exploratory drilling process and assessment of inferred resources, as part of its response to this comment.

Comment 1 from the Staff’s comment letter dated February 18, 2025, states, in relevant part: “Explain in further detail the estimation methodologies employed and geologic data considered in determining inferred resources with reasonable certainty to include them in your resource and reserve base. Please include details such as drill hole spacing and differences in confidence levels between the inferred versus indicated categories.”

The Company advises the Staff that it misinterpreted the Staff’s comment and incorrectly responded in the February 25, 2025 response letter at page 3 that it does not consider the results of drilling in forming its conclusion to include or exclude inferred resources in the resource and reserve base used to estimate the LoM in any given period. The Company confirms to the Staff that, in fact, it does consider drilling evidence and relied on the results of such drilling evidence obtained, in combination with historical drilling results and extensive knowledge of orebody continuity and geological predictability, as its basis to reach the conclusion regarding the inclusion of inferred resources in estimating its LoM as of December 31, 2023. In this regard, the Company seeks to clarify its prior response in three categories as follows:

| A. | Application of IFRS accounting standards regarding drilling evidence obtained. The Company sets forth in Section A below an explanation of the drilling evidence obtained and how such evidence was utilized to form a conclusion regarding the inclusion of inferred resources in the estimate of LoM as of December 31, 2023, in accordance with the principles embodied in IAS 16 and IAS 10. |

| B. | Drilling evidence and reliability of inferred resources. Section B includes a detailed discussion of the extensive exploratory drilling evidence obtained by the Company regarding the inferred resources. Reference is also made to the information included in the Appendices hereto. |

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 5 of 16

| C. | Geological predictability and orebody continuity. In Section C, the Company provides information on the geological predictability and orebody continuity, and how such information supported its conclusion to include inferred resources in its LoM. |

In addition, in consideration of the further review, the Company advises the Staff that it is enhancing its disclosure in Note 3.3 to Greenstone’s financial statements, as incorporated in Amendment No. 4, with respect to the basis of including inferred resources in the LoM, aligning with accounting principles as set forth in IAS 16. The revised Note 3.3 is included under Section A below.

| A. | Application of IFRS accounting standards regarding drilling evidence obtained. |

As a result of the Company’s policy to estimate the LoM utilizing resource and reserve data on a one-year lag basis (i.e., the Company’s December 31, 2023 LoM estimate in the calculation of depreciation is prepared using 2022 resource and reserve data), the Company has the ability to obtain significant levels of either confirmatory or contradictory evidence (through subsequent drilling) regarding the amount of inferred resources reported, prior to the issuance of its annual financial statements:

| ● | As of December 31, 2023, further confirmatory evidence was obtained through the Company’s process of continuous drilling. The latter resulted in the upgrade of 61% of the inferred resources estimated as of December 31, 2022, to indicated and measured resources and provided the Company with evidence that a reasonable expectation of such resources will be upgraded and form part of the eventual extraction. |

| ● | In accordance with IAS 10, which requires adjustments to financial statements when information is obtained after the reporting period and provides new information about conditions which existed as of the end of the reporting period, the Company evaluated any and all new information obtained which may impact an estimate made as of the balance sheet date through the date of issuance of the financial statements. In the period between December 31, 2023 and the date the financial statements were issued on September 12, 2024, the Company’s continued drilling in 2024 provided continued evidence that a high degree of the inferred resources would continue to be upgraded (i.e., an amount greater than the 61% which was upgraded as of December 31, 2023). |

| ● | The Company’s determination to include 3.25Mt of inferred resources in the estimate of the LoM as of December 31, 2023, was based on a combination of historical drilling results which the Company has detailed in previous letters, and the 2023 drilling data noted above which became available prior to the issuance of the audited annual financial statements as of and for the year ended December 31, 2023 and provided confirmatory evidence that a high degree of probability existed that the inferred resources would be upgraded and form part of eventual extraction, consistent with the Company’s historical results. |

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 6 of 16

| ● | As demonstrated by the calculations contained within the confidential supplemental information provided to the Staff in response to Comment 1, the exclusion of these inferred resources would have resulted in a significant reduction in the LoM, and a depreciation policy which the Company believes would not have faithfully represented the pattern of consumption and future economic benefits in accordance with IAS 16. |

| ● | Based on the Company’s evaluation of all available evidence as of the issuance of its December 31, 2023 annual financial statements, the Company believes the inclusion of inferred resources in deriving the LoM estimate as of December 31, 2023 provides a more reasonable reflection of the period over which its mining assets will provide economic benefits than if such resources were fully excluded. In accordance with IAS 16 requirements, the Company will continue to perform an annual re-assessment of its depreciation policy on an annual basis to ensure the method of depreciation appropriately reflects the pattern in which the asset’s future economic benefits are expected to be consumed. |

Revision of Note 3.3 to Financial Statements:

The Company advises the Staff that it is enhancing its disclosure in Note 3.3 to Greenstone’s financial statements, as incorporated in Amendment No. 4, with respect to the basis of including inferred resources in the LoM, aligning with accounting principles as set forth in IAS 16 as follows (changes noted in italics for emphasis):

“The Group estimates the LOM using mineral resources and reserves expected to be derived from the mine and its expected rate of production. Mineral resources and reserves are categorized and reported in compliance with the United States Securities and Exchange Commission’s Subpart 1300 of Regulation S-K (“S-K 1300 Report”). The Group includes inferred resources in the resource and reserve base used to estimate the LOM when the Group holds a reasonable expectation that such resources will be upgraded to indicated and measured mineral resources and form part of eventual extraction. Due to the timing of when the S-K 1300 Report is finalized as compared to the timing of management’s preparation of its annual financial statements, the LOM is estimated using resource and reserve data on a one-year lag basis. Accordingly, the LOM estimate as of December 31, 2023, is prepared with 2022 resource and reserve data.

As of December 31, 2023, the Group estimates the LOM for the How Mine to be 8 years. In forming the estimate, the Group included in the portion of mineralization expected to be classified as reserves 3.25Mt of inferred resources. The Group’s determination to include the specified amount of inferred resources was formed on the basis of historical drilling results which have yielded continuous high rates of conversion, and current year drilling results which provided confirmatory evidence and a high degree of confidence that over time a significant amount of prior year measure of inferred resources utilized to form the December 31, 2023 estimate (one-year lag basis), would be upgraded and form part of the eventual extraction. The Group determined based on its evaluation of all available evidence and data, that the inclusion of the inferred resources would most faithfully represent the pattern of consumption and future economic benefits in accordance with IAS 16.

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 7 of 16

With respect to the Group’s Mazowe and Redwing Mines, the Group has no assets subject to LOM depreciation due to the closures of each mine and the related impairments. Refer to Note 13 for additional discussion.

Depreciation methods, useful lives and residual values are assessed for appropriateness at each reporting date and adjusted if necessary.

Refer to policy Note 3.10 below for discussion on the Group’s impairment policies.”

| B. | Drilling evidence and reliability of inferred resources |

The Company advises the Staff and confirms that its inferred resources are not assumed to convert automatically based on expectations alone but is supported by the data and information from a structured drilling program at the How Mine.

The historical resource conversion trends from the 2022 to 2023 data and information indicate the following based on the table included below:

| ● | 61% of the 2022 inferred resources were upgraded to measured and indicated resources during 2023. |

| ● | This transfer fundamentally provides evidence that within only a one-year period from reporting the inferred resources of 3,254kt that 1,975kt moved during the 2023 financial year to resources that are measured and indicated. |

| ● | The Company considers that this provides the highest level of confidence that this tangible information subsequent to the 2022 financial year-end, which is based on actual drilling program results, provides evidence to support the estimate of the high probability that the inferred resources do exist and that the Company will be able to extract these resources throughout the life of the mine. |

| ● | The Company had access to these actual drilling results prior to the time the 2022 and 2023 annual financial statements were issued in September 2024. As a result, this information of actual events subsequent to 2022 allowed the Company to draw an appropriate conclusion on including the inferred resources to determine the LoM. |

| ● | The Company advises the Staff that it, therefore, considers the inclusion of the inferred resources to establish an 8-year LoM to be appropriate, especially given that within only one year, 61% of those inferred resources were already upgraded. |

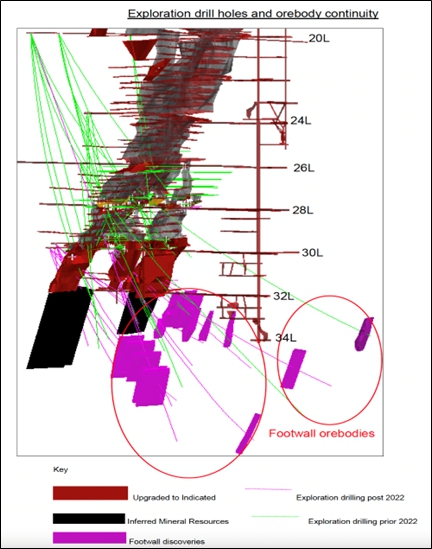

| ● | A further 731kt of inferred resources were discovered in the footwalls of known orebodies through exploratory drilling during 2023, demonstrating the potential of the mine to expand its resource base and therefore LoM and further supports the mineralization beyond the previously defined limits. |

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 8 of 16

The information in the table below supports the fact that inferred resources in 2022 were upgraded to measured and indicated resources in 2023. These results are derived from the Company’s ongoing exploratory drilling program, described below.

| Resource Category | 2022 (kt) | 2023 (kt) | Net Change (kt) | |||

| Reserve | 760 | 840 | +80 | |||

| Measured & indicated | 621 | 2066 | +1,445 | |||

| Inferred | 3,254 | 2010 | -1,244 | |||

| Total Resources | 4635 | 4916 | 281 |

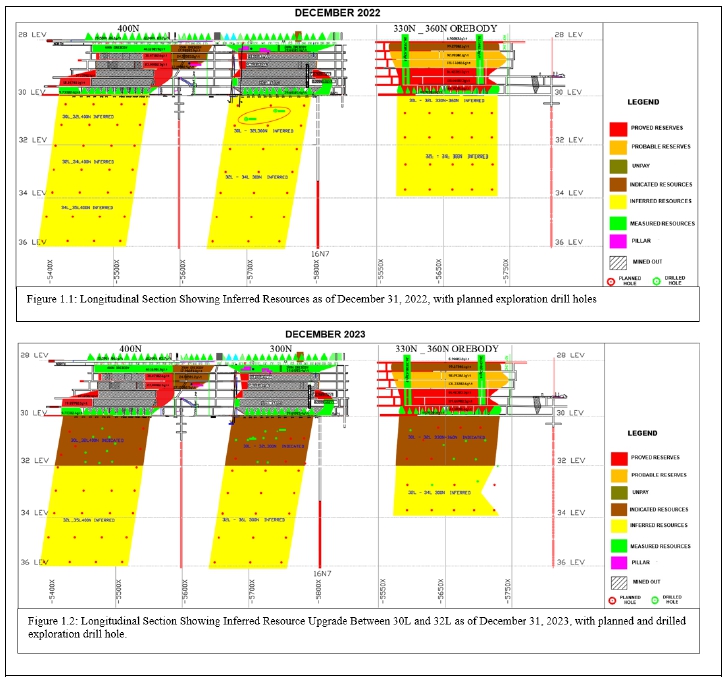

Inferred resources are generated by interpretation of the information obtained from ongoing exploration, combined with the intimate knowledge of orebody characteristics. Please see Figures 1.1 and 1.2 in Appendix A for a pictorial representation of the upgrading of inferred resources between year-ends 2022 and 2023. This data has been independently reviewed and verified. Set out below is further information on the Company’s exploratory drilling program in 2023 and 2024:

| ● | 6,946 meters were drilled in 2023, targeting resource upgrades. This drilling was done during the 2023 financial year providing a high level of confidence around the inclusion of the inferred resources in the LoM. |

| ● | 7,919 meters were drilled in 2024, focusing on resource upgrades. |

| ● | The exploration drill holes are spaced on a grid of 25m along the orebody length and 30m on orebody. See Figure 2.1 in Appendix B noting this grid for resources upgrade from Inferred to Indicated. |

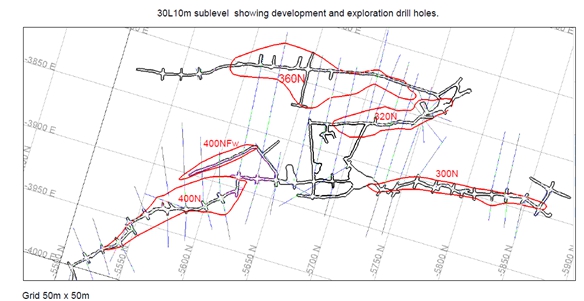

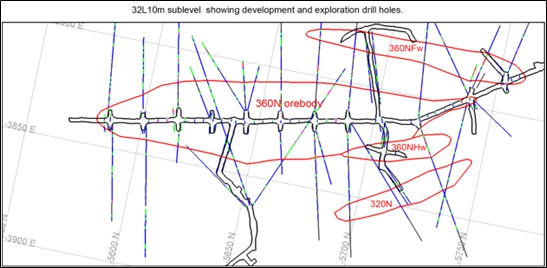

| ● | Development and sublevel exploration drilling are done at a grid of 15m along the orebody length and 10m on orebody inclination depth. Please see Figure 3.1 in Appendix C and Fig. 3.2 in Appendix D, which note this grid for detailed upgrading. |

| C. | Geological predictability and orebody continuity |

In addition to the actual drilling results during 2023, the Company advises the Staff that the How Mine is part of a regionally continuous, structurally controlled gold system, which provides further evidence of the high probability of inferred resources being a justifiable extension of known mineralization.

The Company advises the Staff that the How Mine is located within the Bulawayo Greenstone Belt, a well-documented Archean-aged gold-bearing geological structure that has demonstrated long-term mineralization continuity. The Bulawayo Greenstone Belt has the following characteristics:

| ● | Host Rock Formations: The deposit is hosted in talc-chlorite schists, banded iron formations (BIFs), quartz-sericite schists, and siltstones, all of which provide a stable geological setting for gold mineralization and facilitate deep mineralization persistence. Furthermore, the Company notes that, prior to 2022, there were two exploratory drill holes (which has been independently reviewed and verified) that pierced the 300N orebody around 31L during the 2002-2005 drilling campaign, which confirmed continuity of orebodies on the down dip. Please see Figure 1.1 in Appendix A. |

| ● | Structural Controls: Gold mineralization is associated with high-angle, steeply dipping shear zones (70°–80°W) that act as conduits for hydrothermal fluids. These structures have remained stable over geological time, demonstrating consistent mineralization patterns across mining levels. |

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 9 of 16

| ● | Regional Comparisons: Blanket Mine (Caledonia Mining) which is also within the Bulawayo Greenstone Belt has defined resources up to 1,500m (42 Level), demonstrating that these shear-hosted systems are geologically continuous at depth. Additionally, historical deep mines in the region, such as the Mponeng Mine, have reached depths exceeding 4,000m, confirming the viability of deep mineralization. |

| ● | Predictable Orebodies Shape and Boundaries: The orebodies have a combined strike length of 500m, with no evidence of structural termination, further reinforcing its predictable extension potential. |

| ● | New Orebodies Discoveries: Recent exploration drilling in 2023 identified 731kt of inferred resources in the footwall zones, confirming the presence of mineralization beyond previously defined limits. Please see Figure 2.1 in Appendix B. |

Bulawayo Greenstone Belt’s shear-zone-controlled orogenic gold deposits historically have been mined to significant depths across similar regional operations. Specifically, the How Mine shear zone was extensively mapped to 800m below mean sea level, which corresponds to 2,086m below the current How Mine surface shaft bank (Garson, 1995: Geological Bulletin No.93). This mapping confirmed continuity of the shear zone that hosts the mineralization. Currently, the How Mine inferred resource is defined down to 1,320m below the current How Mine surface shaft bank and exhibits similar structures to those mapped by Garson.

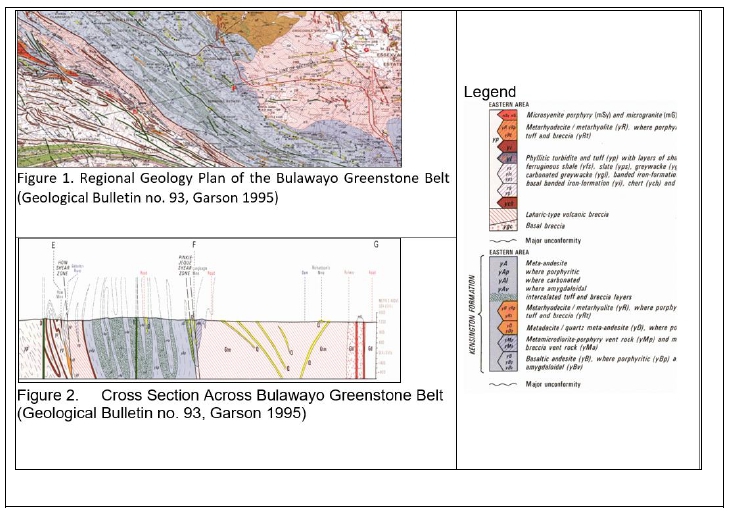

This demonstrates that the How Mine shear zone is mapped far below the current lowest boundary of the inferred resource and indicates that the actual LoM has potential to exceed the currently estimated LoM. Please see Figure 1 in Appendix E, which is extracted from the Geological Bulletin No. 93 and shows the regional geology around the How Mine, and Figure 2 in Appendix E, which shows the position of the How Mine (located at position E of Figure 2) within the How Mine shear zone of the Umzingwane formation.

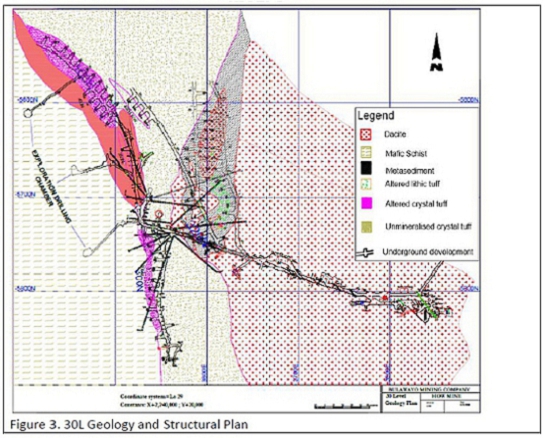

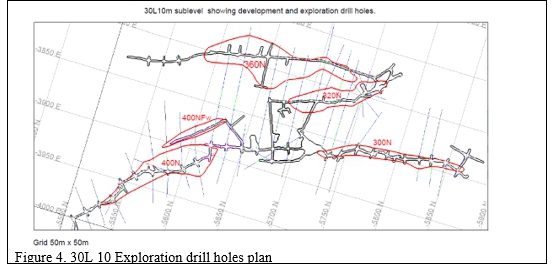

As of December 31, 2022, the defined inferred resources were lying below 30L. The mining lift between 30L and 28L had extensive development, exploration drilling and mapping carried out to define measured resources which were subsequently extracted (see Figures 3 and 4 below in Appendix F). The orebodies were strongly defined within the How Mine shear zone, exhibiting similar geometry and geological structures on strike and dip. Continuity of the structures and mineralization could be observed in the down dip. Exploration drilling chambers were also established for continual exploration testing of the down dip extensions of the orebodies below 30L.

* * * * * * * * * *

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 10 of 16

We thank the Staff for its continued assistance and cooperation throughout the course of the review of the Registrants’ Registration Statement, including the Staff’s availability for discussion of these matters and its consideration of the Company’s foregoing responses to the Comment Letter. If the Staff requires any additional information or has any questions regarding the foregoing responses, please do not hesitate to contact the undersigned at (310) 586-7773 or by email at Barbara.Jones@gtlaw.com. As noted above, the Registrants intend to seek acceleration of the Registration Statement as soon as possible.

| Very truly yours, | |

| GREENBERG TRAURIG, LLP | |

| /s/ Barbara A. Jones | |

| Barbara A. Jones, Esq. |

Attachments: Appendices

| cc: | Office of International Corporate Finance, Securities and Exchange

Commission John Coleman, Division of Corporation Finance, Office of Energy & Transportation, |

|

| Securities and Exchange Commission | ||

| Ibrahima Tall, Chief Executive Officer, Namib Minerals | ||

| Tulani Sikwila, Chief Financial Officer, Greenstone Corporation | ||

| Siphesihle Mchunu, General Counsel, Namib Minerals | ||

| Alan Annex, Greenberg Traurig, LLP | ||

| Adam Namoury, Greenberg Traurig, LLP |

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 11 of 16

APPENDIX A

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 12 of 16

APPENDIX B

Figure 2.1: Down Dip Exploration: The exploration drill holes are spaced on a grid of 25m along the orebody length and 30m on orebody.

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 13 of 16

APPENDIX C

Figure 3.1: Development and sublevel exploration drilling done at a grid of 15m along the orebody length and 10m on orebody inclination depth for 30L 10m and 32L 10m.

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 14 of 16

APPENDIX D

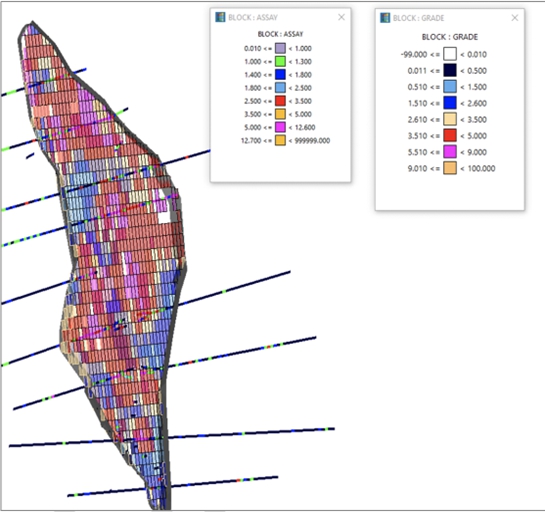

Figure 3.2: 29L 330N Block Grade Drill hole comparison.

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 15 of 16

APPENDIX E

U.S. Securities and Exchange Commission

Division of Corporation Finance

March 10, 2025

Page 16 of 16

APPENDIX F